The Downfall of the Starter Home: A Case for Paying More Now

I had a conversation with a client the other day about amortizing loans and the effects of additional principal payments on total interest paid over the life of the loan. We also discussed the hidden interest costs of resetting the amortization schedule by selling and buying another house in before the loan has been paid in full.

At a really high level, I knew that the payments at the beginning of the amortization schedule go primarily to interest (say 95% interest, 5% principal), and shift towards principal over time (ending around 10% interest and 90% principal). But was there any benefit to paying down principal if you were only going to hold the property for 5-10 years?

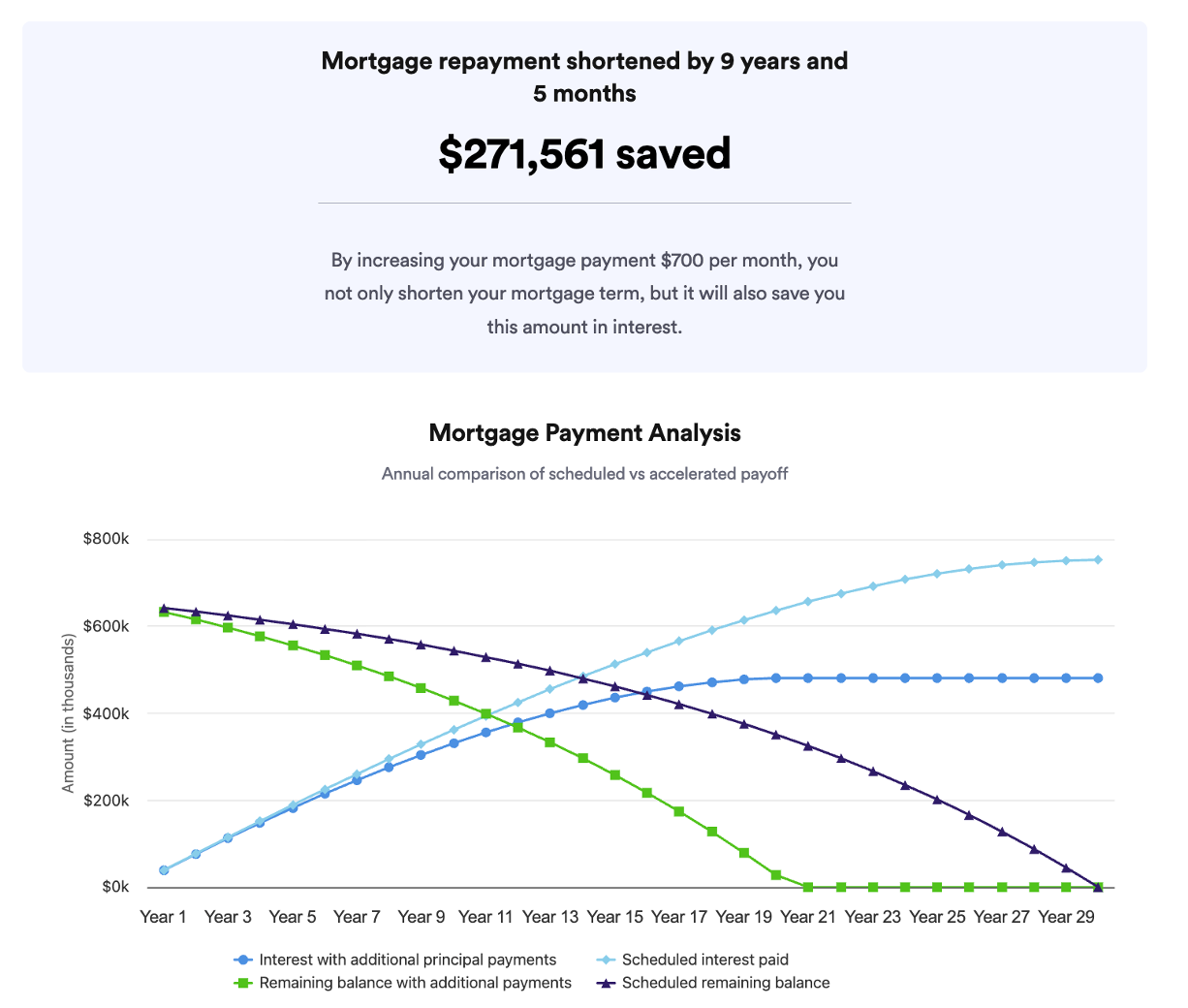

First, I found a website that plots the effect of additional payments on both principal pay down and total interest paid over the course of the loan. Here is an example of what happens if you make additional principal payments over the life of the loan.

At first glance, the interest rate savings during the first ~5 years appears relatively negligible. This is the difference between the two blue lines. Even at year 10 the benefit is not that significant. It's only in year 15-19 that they really diverge, and yield the most benefit to the buyer.

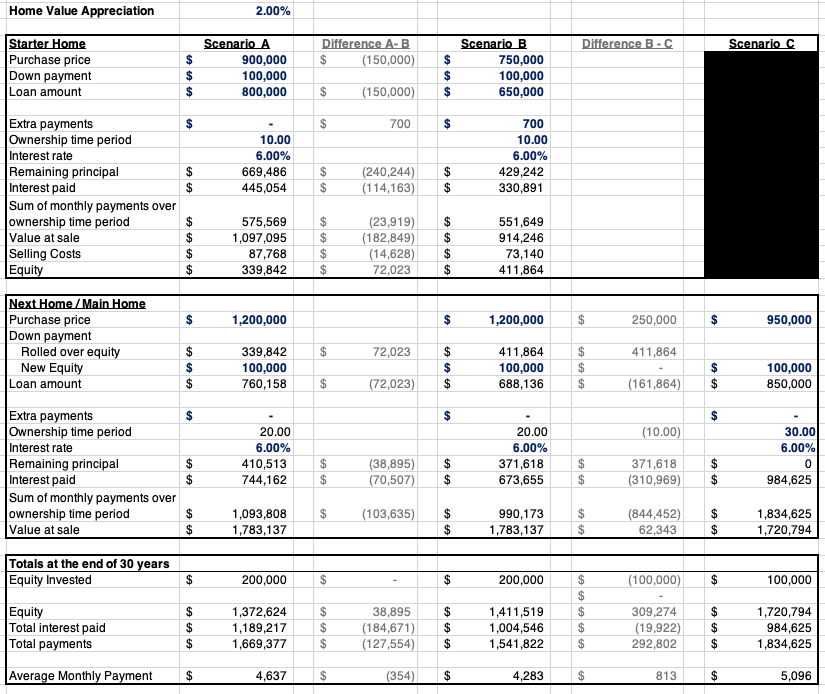

What my client proposed actually went one step further than this, though, and asks what the difference in interest rate expense would be if a buyer made extra payments and started with a smaller loan amount, i.e. they bought a starter home first, aggressively paid down principal, and then bought their forever home later down the road. I was also curious if resetting the amortization schedule had a meaningful impact on total interest paid, so I built a model to analyze all three variables. The model looks at three scenarios:

Scenario A: A moderately expensive initial purchase, held for 5-10 years, then a new home purchase that's 25-30% more expensive than the initial home(adjusted for inflation), held for the remainder of 30 years

Scenario B: A slightly less expensive initial purchase, held for 5-10 years, with an additional $700/mo payment towards principal, then a new home purchase that's 25-30% more expensive than the initial home(adjusted for inflation), held for the remainder of 30 years.

Scenario C: Most expensive initial purchase, held for 30 years, no additional principal payments.

Each scenario assumes 2% home value appreciation, and a 6% interest rate on all loans. Scenario A and B assume the buyer contributes the equity from the first house into the second as well as an additional $100,000. Here is my takeaway:

Despite starting with the highest loan amount and requiring the least amount of total equity, Scenario C ended up with the lowest total interest paid.

The equity earned in Scenario C is 22% higher than Scenario B and 25% higher than Scenario A. The tradeoff is higher average monthly payments. Also surprising because the model requires the owner to contribute an extra $100,000 down payment at year 10.

During the first 10 years, Scenario B incurred 26% less interest than Scenario A ($330,891 vs. $445,054. About 75% of the savings came from the lower purchase price, with only 25% coming from the additional principal payments.

It’s aso worth pointing out that in Scenario A&B, a balance still remains on the mortgage, where as the property is paid in full in Scenario C.

In a rapidly appreciating market with low interest rates, less expensive properties are an effective way to keep short term costs low and see meaningful bumps in your equity. However, with expensive financing and the knowledge that you will surely be buying again in the future, the math makes a convincing argument for buying a larger, more expensive property that you can own for the longest amount of time possible.

As the old adage goes: Buy Once, Cry Once.

If you want to play around with different scenarios, here are two different tools I found:

https://www.bankrate.com/mortgages/additional-mortgage-payment-calculator/

https://www.oakstarbank.com/calculator/mortgage-loan

Feel free to send me an email if you’d like a copy of the worksheet.